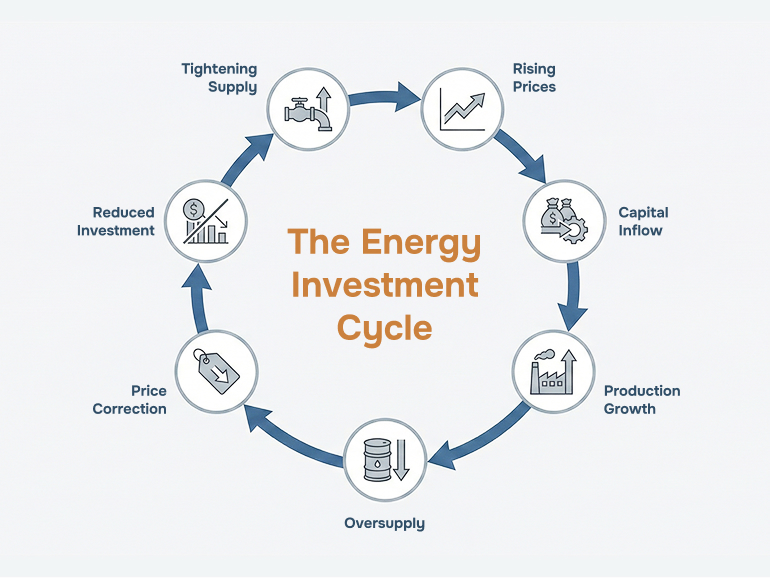

Energy markets have historically moved in cycles.

Periods of tight supply and rising prices are followed by expansion, increased production, and eventual oversupply. Weak markets often lead to capital restraint, which can contribute to conditions that support recovery over time. This rhythm has defined the oil and gas industry for decades.

Understanding this pattern is different from trying to predict the next price move.

For long-term investors, recognizing how cycles function may be more durable than attempting to forecast where prices may move next quarter.

Why Energy Markets Move in Cycles

Energy is a capital-intensive business with long development timelines. Bringing new oil or natural gas supply online can take years—from exploration and permitting to drilling and infrastructure buildout.

When prices rise, capital flows into the sector. Production expands—but not immediately. By the time new supply reaches the market, market conditions may have changed.

Conversely, when prices fall, companies reduce spending. Supply may tighten over time, which has historically contributed to subsequent recoveries.

Historical production and capital expenditure data from the U.S. Energy Information Administration’s Petroleum & Other Liquids datasets show this delayed response clearly in upstream oil and gas activity.

What Drives Energy Market Cycles

While each cycle has unique features, several structural forces consistently influence outcomes:

Supply Response Lag

Energy production does not adjust instantly. Investment decisions made today may not impact supply for several years.

Demand Sensitivity to Growth

Global energy demand is closely tied to economic activity, industrial production, and population growth. Long-term outlooks from the International Energy Agency (IEA) World Energy Outlook consistently highlight this relationship between GDP growth and energy consumption.

Capital Allocation and Returns

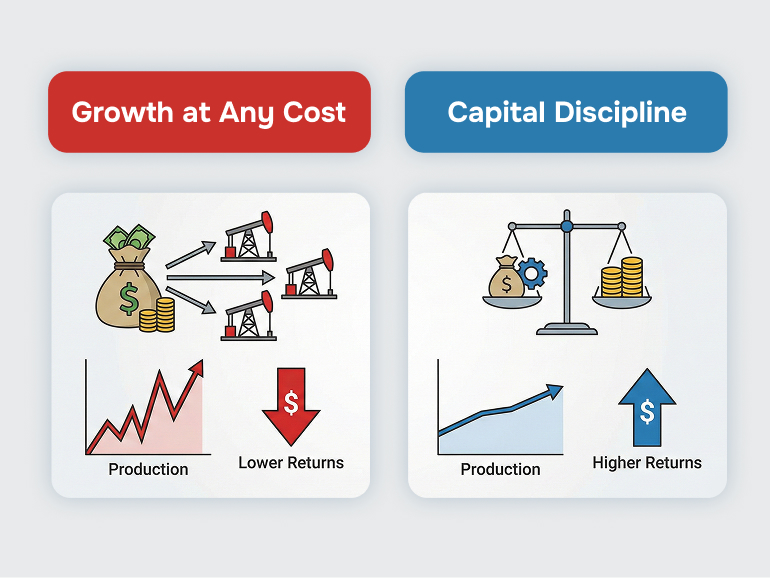

In prior decades, aggressive production growth often took priority over returns. More recently, producers have emphasized capital discipline—focusing on cash flow, balance sheets, and shareholder returns.

Public company filings and industry aggregate data reflect this structural shift in capital allocation behavior.

The Role of Capital Discipline

.Over the last decade, many producers have shifted from prioritizing rapid volume growth to prioritizing return on capital and free cash flow generation.

Industry data tracked by the EIA shows that capital spending has not risen proportionally with commodity price recoveries in recent cycles. This restraint reflects a broader emphasis on balance sheet repair and shareholder returns.

When companies limit spending during periods of stronger prices, supply growth may be more measured. That may moderate the amplitude of cycles over time.

Understanding this evolution is more useful than attempting to forecast specific price levels.

Volatility vs. Long-Term Value

Commodity prices are inherently volatile. Oil and natural gas markets respond quickly to geopolitical events, economic data, weather patterns, and policy changes.

Short-term price movements can be sharp. For example, historical crude oil price data published by the EIA shows multiple periods of rapid increases and declines within single-year timeframes.

But long-term value creation in energy companies is driven by:

- Cost structure

- Asset quality

- Balance sheet strength

- Capital allocation discipline

- Operational efficiency

Investors focused on these structural elements are less dependent on predicting commodity prices precisely.

Investing With Discipline, Not Forecasts

Forecasting energy prices is inherently uncertain. Even institutions regularly revise outlooks in response to new data.

What is more observable are the mechanics of the cycle:

- Capital spending trends

- Production growth rates

- Inventory levels

- Balance sheet health

- Corporate return strategies

Long-term investing in energy is not about predicting peaks and troughs. It is about understanding where we are in the cycle and evaluating whether companies are positioned to navigate it responsibly.

Energy cycles have historically persisted and may continue in the future. The focus is less on whether volatility may occur—and more on how capital is managed through it.

Disciplined operators and disciplined investors both recognize the same principle:

Cycles reflect structural dynamics. Price predictions are not required for long-term analysis.

Resources

U.S. Energy Information Administration – Petroleum & Other Liquids Data

Comprehensive historical data on crude oil production, prices, and capital activity.

https://www.eia.gov/petroleum/

International Energy Agency – World Energy Outlook

Long-term global energy demand and supply projections.

https://www.iea.org/reports/world-energy-outlook

These resources are provided for general education and independent research. They are not intended as market forecasts or investment guidance.