Energy plays a central role in the global economy. It powers transportation, industry, and daily life. At the same time, it is one of the more cyclical and variable sectors in financial markets.

Setting realistic expectations starts with understanding both sides: energy’s long-term importance and its natural ups and downs.

Energy Is Built Around Cycles

Energy markets are closely tied to commodities like oil and natural gas. These prices move in real time and can shift quickly based on supply, demand, and external factors like weather or policy.

Because of this, volatility is a normal part of how the sector functions, not an exception.

Over time, investment in energy has also followed cycles. Periods of higher spending are often followed by pullbacks, depending on market conditions.

Performance Changes Over Time

Energy does not tend to move in a straight line.

There have been periods where the sector has lagged broader markets, as well as periods where it has outperformed. These shifts are often tied to supply-demand balances and broader economic conditions.

Looking at energy through a longer-term lens can help put these cycles into context.

Investment Is Evolving

Energy investment today is changing, not disappearing.

Global spending remains significant, with capital flowing into both traditional energy sources and newer technologies. In many cases, companies are focusing on:

- Lower-cost opportunities

- Shorter development timelines

- More efficient operations

This reflects a more measured approach compared to past cycles.

Common Expectation Gaps

Some expectations can make the sector harder to understand:

Assuming steady returns

Energy has historically moved in cycles rather than delivering consistent performance year to year.

Focusing only on short-term prices

While commodity prices matter, many investment decisions are based on longer-term assumptions.

Overlooking differences within the sector

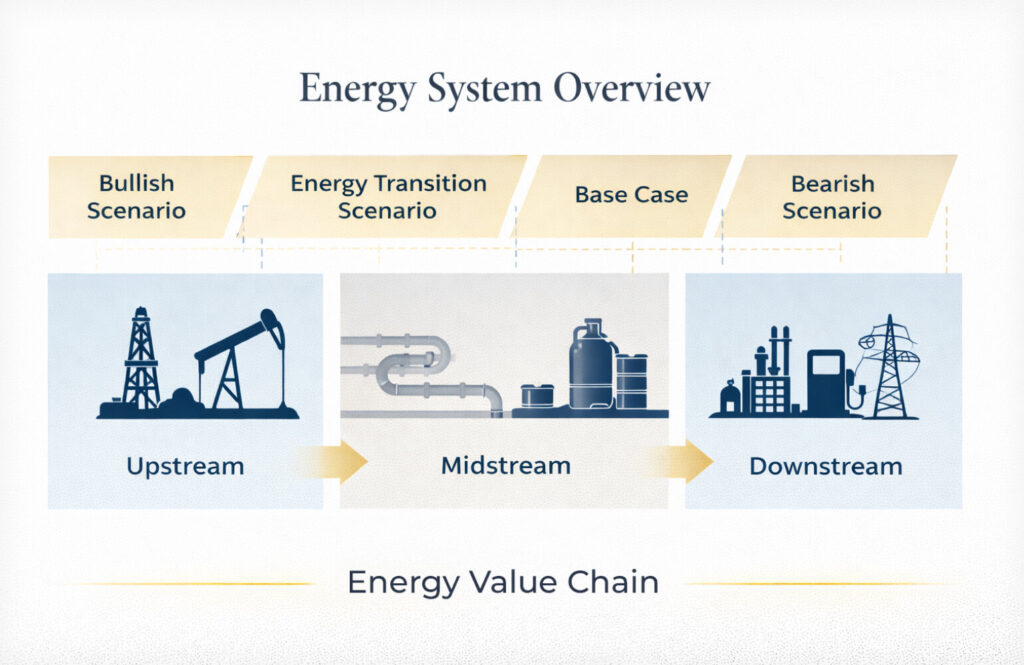

Upstream, midstream, and downstream businesses can behave very differently in terms of stability and returns.

Building a More Balanced View

A more grounded perspective often includes a few key ideas:

Time horizon matters

Short-term results can vary widely, while longer periods may reflect broader cycles.

Different outcomes are possible

Many institutions use multiple scenarios to account for uncertainty in demand, policy, and technology.

Not all energy assets are the same

Different parts of the value chain can offer different risk and return profiles.

The system is adjusting over time

Traditional energy remains essential, while new sources continue to grow alongside it.

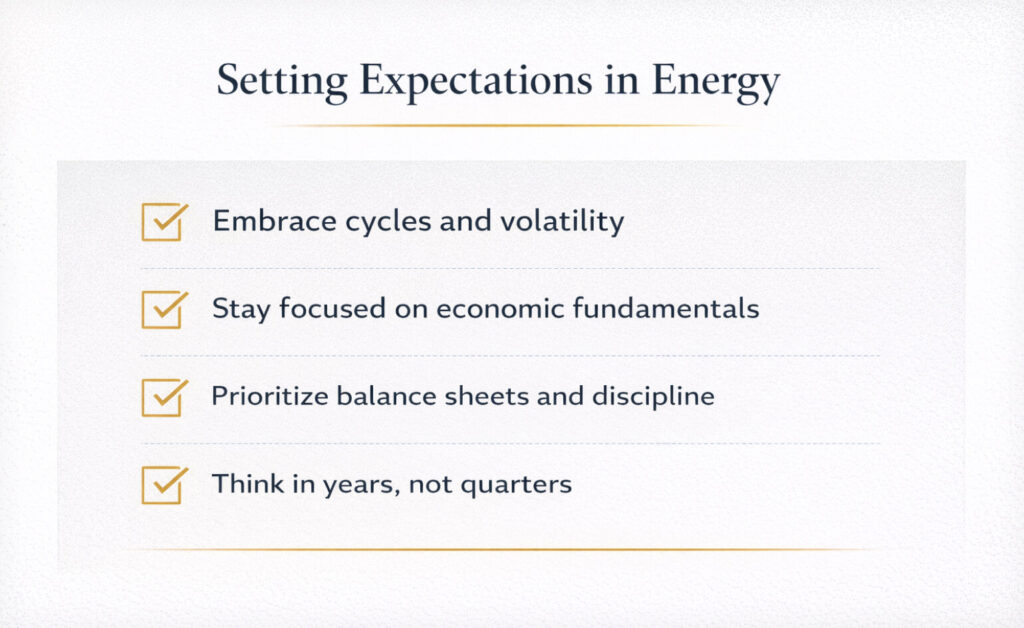

A Practical Way to Think About It

A simple framework for setting expectations in energy:

- The sector has historically been more volatile than the broader market

- Performance has tended to follow cycles rather than steady growth

- Outcomes can vary based on timing, structure, and asset type

- Long-term positioning often matters more than short-term movements

Understanding these patterns can make the sector easier to evaluate over time.

Resources

International Energy Agency – World Energy Investment

Global view of energy capital flows across traditional and emerging sources

https://www.renewableinstitute.org/global-energy-investment-hits-record-high-key-takeaways-from-the-ieas-2025-report/

Fortum – “Sure, volatility is here to stay”

Explains structural drivers of persistent energy market volatility

https://www.fortum.com/news-and-publications/forthedoers-blog/sure-volatility-here-stay-it-doesnt-have-be-risk

ScienceDirect – Volatility modeling in energy markets

Academic perspective on persistent and clustered commodity volatility

https://www.sciencedirect.com/science/article/pii/S0306261926002114

IEEFA – Fossil fuel stock performance

Historical analysis of energy sector returns and volatility

https://ieefa.org/articles/another-bad-year-and-decade-fossil-fuel-stocks

DW Energy – Energy cycles and long-term value

Explores cyclical nature of energy investing and long-term positioning

https://www.dwenergygroup.com/energy-cycles-and-long%E2%80%91term-value-in-oil-and-gas-investing/