U.S. crude oil production remains one of the most closely watched variables in global energy markets. Because the United States is both a major producer and exporter, even modest changes in its supply outlook can influence infrastructure planning, trade flows, and broader market expectations.

The most recent Short-Term Energy Outlook from the U.S. Energy Information Administration (EIA) provides updated projections for how U.S. crude oil production may evolve over the next several years. Rather than pointing to rapid growth or sharp contraction, the forecast reinforces a theme that has been emerging more clearly in recent data: U.S. oil production is projected to remain relatively stable over the forecast period.

This post uses the EIA’s latest forecast as context to explain what is driving that outlook, how regional trends factor in, and how this stability fits into near-term supply fundamentals.

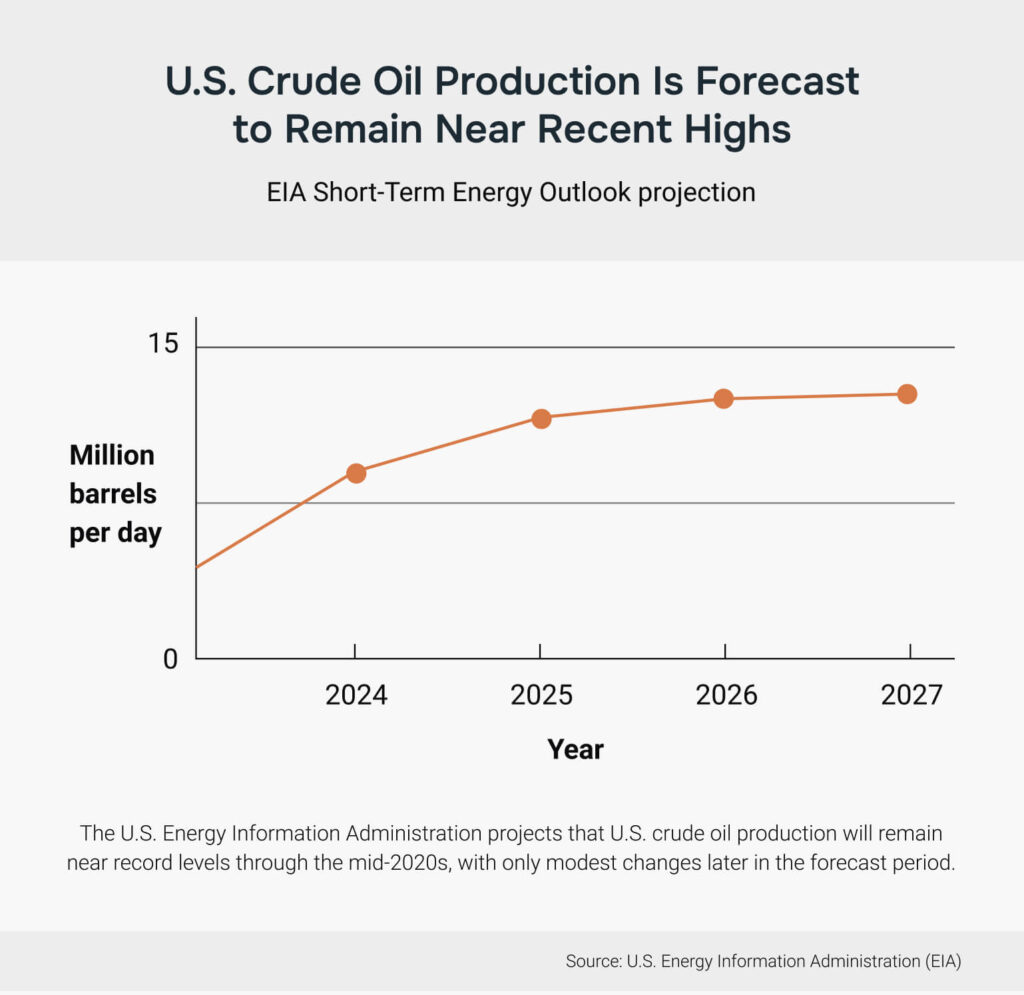

A Production Profile That Is Leveling Off

According to the EIA, U.S. crude oil production is expected to remain near record levels through 2026, followed by a modest decline in 2027. The most important takeaway is not the precise year-to-year changes, but the broader pattern: production is forecast to plateau rather than continue the rapid growth seen in earlier years.

By historical standards, these volumes remain high. The United States is projected to sustain output levels that would have been considered exceptional just a decade ago. What has changed is the pace of growth. Instead of consistent year-over-year increases, the outlook points to maintenance of existing capacity with gradual adjustments over time.

This shift reflects a maturing production system rather than a sudden structural break.

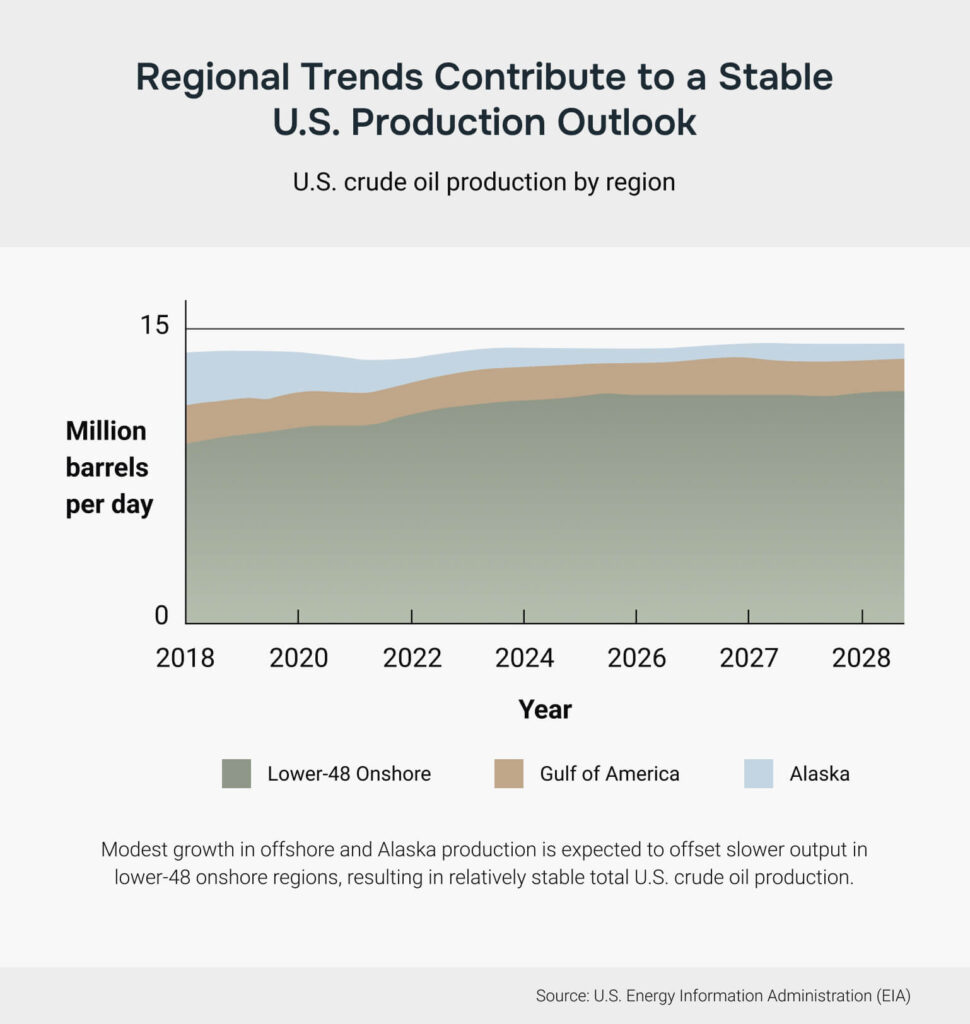

Regional Differences Shape the National Outlook

The EIA forecast highlights how national production totals are the result of offsetting regional trends.

In offshore regions such as the Gulf of America, as well as in Alaska, production is expected to grow modestly. These areas are characterized by long project lead times, meaning current output reflects investment decisions made years earlier. As a result, production in these regions tends to be less sensitive to short-term price movements.

By contrast, lower-48 onshore production is projected to slow. Onshore shale regions respond more quickly to market conditions, and lower crude prices have contributed to reduced drilling activity. Over time, fewer new wells translate into slower production growth as declines from existing wells take effect.

The combined effect of these regional trends is a relatively flat national production profile with gains in some regions offset by softness in others.

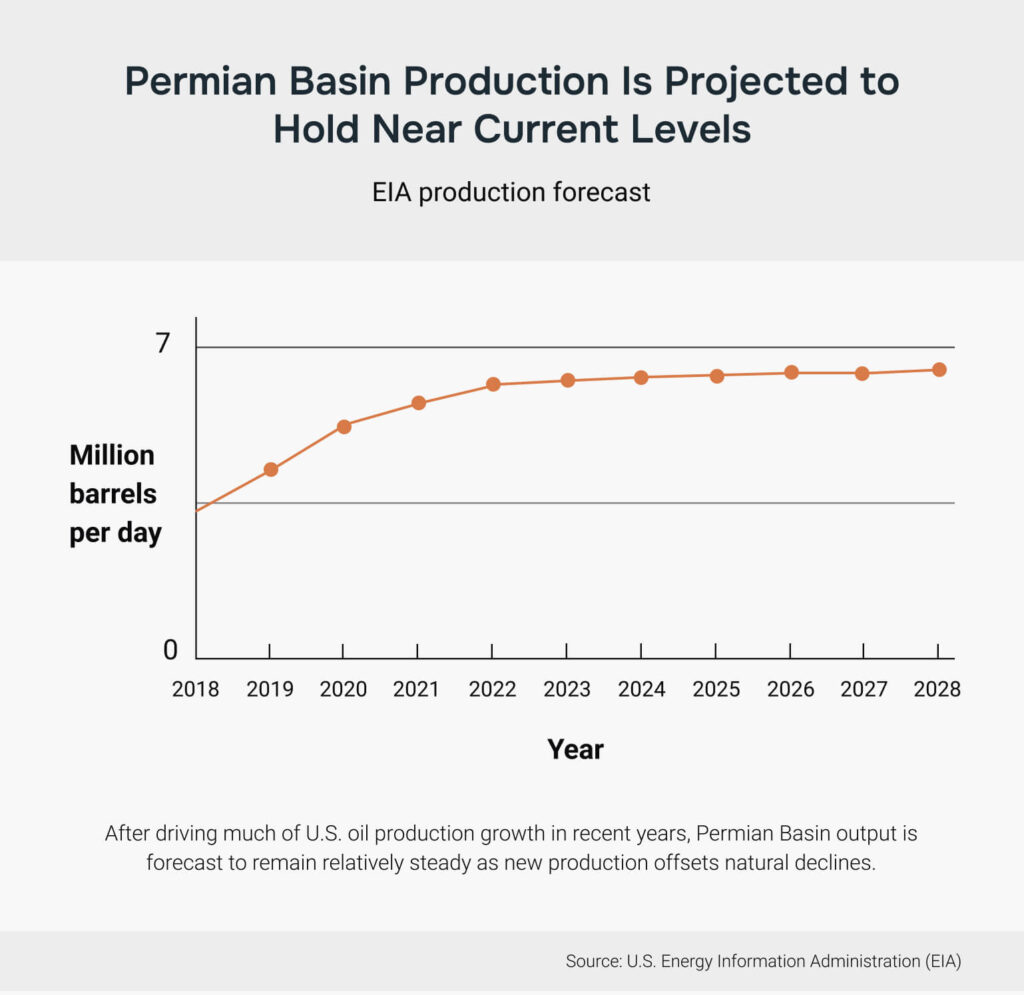

The Permian Basin’s Transition From Growth Engine to Anchor

The Permian Basin has played a central role in U.S. oil production growth over the past decade, making its outlook particularly important. The EIA projects that Permian production will hold close to 2025 levels rather than continue expanding at earlier rates.

This does not indicate a loss of importance. The basin remains one of the most productive and efficient oil-producing regions in the world. Instead, it suggests that development has entered a more mature phase. Incremental gains from new drilling are increasingly balanced by natural declines from existing wells and by more selective capital deployment.

In this context, the Permian functions less as a driver of rapid growth and more as a source of stable supply..

Prices, Investment, and Capital Discipline

Another factor underlying the forecast is the price environment assumed in the outlook. Lower expected crude prices tend to reduce incentives for aggressive drilling particularly in plays with higher marginal costs.

In recent years, many producers have emphasized capital discipline, focusing on maintaining production, improving efficiency, and managing balance sheets rather than maximizing output growth. This approach tends to produce steadier supply outcomes, dampening both surges and steep declines.

The EIA’s projection reflects these dynamics, assuming that operators will largely continue to align activity levels with price signals and capital constraints.

What a Stable Supply Outlook Implies

From a fundamentals perspective, a period of stable U.S. oil production carries several implications.

First, changes in global oil supply are likely to be driven more by developments outside the United States, including OPEC+ policy decisions, geopolitical risks, and production trends in other major producing countries.

Second, stable production supports more predictable utilization of infrastructure such as pipelines, export terminals, refineries, and storage facilities. This consistency can be particularly important for long-lived assets that depend on steady throughput.

Finally, inventory levels may become more sensitive to demand fluctuations and seasonal patterns rather than being dominated by rapid supply growth.

Forecasts as Context, Not Certainty

Like all projections, the EIA’s forecast is based on current assumptions about prices, productivity, technology, and policy. Any of these variables could change. Technological improvements could alter well performance, price movements could shift investment behavior, and policy developments could influence production economics.

The value of the outlook lies in the context it provides rather than in precise prediction. It helps frame expectations around what is most likely given current conditions, while acknowledging uncertainty.

A Measured Signal From the Latest Data

Taken together, the latest EIA production forecast points to continuity rather than disruption in U.S. oil supply. Production remains historically high, regional dynamics are balancing one another, and capital discipline is shaping development decisions.

As a piece of context, the outlook suggests that the U.S. oil market is moving through a phase defined less by expansion and more by maintenance — with gradual, incremental changes replacing the rapid growth that once dominated the narrative.

Resources

- U.S. Energy Information Administration (EIA), Short-Term Energy Outlook

- EIA, Today in Energy: U.S. crude oil production forecasts and regional trends

- EIA, Drilling Productivity Report

- EIA, U.S. Crude Oil Production by Region

These resources are provided for general education and independent research. They are not intended as market forecasts or investment guidance.