Nobody commits capital to an investment expecting to lose it.

They go in having done their research. Having spoken to the right people. Having looked at the numbers and felt that this was a sound decision. And then somewhere between the pitch and the reality, something goes wrong. A slow, quiet erosion of what was supposed to happen.

The painful part isn’t the loss. It’s the realisation, months or years later, that the signs were there. That the right questions – asked at the right moment, before the money moved – would have told a different story.

This article is about those questions.

Is the demand actually there – and what does that mean for your investment timeline?

Before anything else, you need to understand the world your capital is entering. Because no amount of operator skill or favorable geology saves your investment if the underlying demand isn’t there to support it when you need cash flow.

Here’s what the headlines won’t tell you: petroleum and natural gas together account for the overwhelming majority of U.S. energy consumption – and that share has remained structurally stable for years. Despite all the transition talk, demand remains robust.

The investors who understand that distinction enter projects with clarity and conviction – knowing their capital is backed by real market fundamentals. The ones reacting to transition headlines enter them with doubt – and doubt at the wrong moment costs you money.

What this means for you: When you commit capital to a long-cycle asset, you’re making a bet that the market will still be there when your production ramps up and your cash flows begin. Macro conviction isn’t background noise – it’s the foundation everything else in your portfolio is built on. Without it, you’re not investing. You’re hoping. And hope doesn’t pay quarterly distributions.

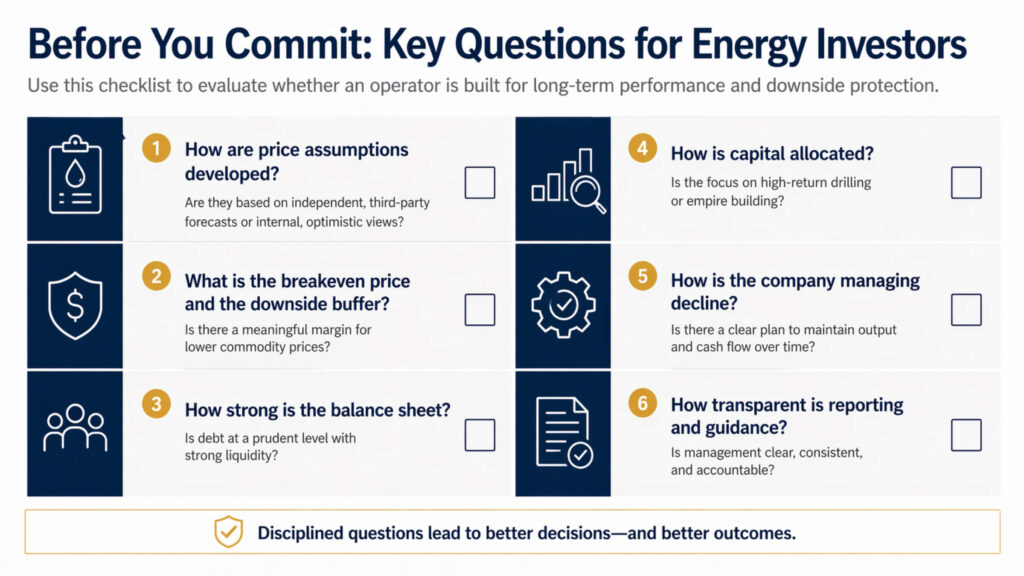

How does the operator make investment decisions – and how does that protect (or expose) your capital?

This is the question almost nobody asks. And it’s the one that tells you the most about your downside risk.

Because an operator’s relationship with risk doesn’t change when your money is on the line. The way they think about downside scenarios, price assumptions, and capital discipline when they’re pitching you is exactly how they’ll think about your investment when conditions get difficult and decisions get hard.

Serious operators don’t build drilling programs around optimistic price forecasts. Research on investment decision-making in the oil and gas sector shows that the most prudent producers use conservative, backward-looking price assumptions – typically a weighted average of recent prices – not projections of where prices might go.

Aggressive assumptions look attractive in a deck. In practice, they’re betting with your principal.

What this means for you: An operator who needs $85 oil to make a project work is asking you to bet your capital on prices going their way. An operator who needs $55 is giving you a buffer – room for the market to move without your returns moving with it. That gap isn’t a technical detail. It’s the difference between you sleeping well and watching commodity prices with one eye open, worried about your investment.

What does the production timeline actually look like – and when will you see returns?

Every oil and gas well follows the same arc: strong early output, then a natural decline as reservoir pressure drops. This isn’t a flaw – it’s physics. But it shapes everything about how your returns actually materialize, and most investors never look closely enough at what the curve looks like beyond year one.

Early cash flow is real. It’s one of the genuine structural advantages of direct participation in oil and gas – money hitting your account, not just paper gains. But that cash flow comes with a built-in decline baked in – and the operator’s plan for what replaces it is just as important to your long-term income as the headline production numbers they lead with.

What this means for you: If you’re evaluating a project on year-one production numbers alone, you’re reading the first sentence and calling it the whole story. The returns that were promised to you were calculated across the full life of the project – not just the exciting early months.

Ask what the decline curve looks like. Ask what the operator plans to do about it. If the answer is vague, your future cash flow is at risk.

What are the actual costs – and how do they protect your margin when prices drop?

Projected returns are always calculated at an assumed price. Your actual returns will be calculated at whatever price the market delivers – which may be very different.

This is why your margin matters more than price. Margin is the gap between what oil sells for and what it costs to get it out of the ground. And that gap is what determines whether your project still delivers when conditions shift.

Historical data on energy investment decision-making shows that well costs and commodity prices tend to rise and fall together – meaning a project that looks profitable at $90 oil may look very different at $65 once you account for the cost environment that accompanies lower prices. And that $65 environment affects your distributions directly.

What this means for you: The wider the gap between breakeven and current price, the more room your project has to absorb market volatility and still generate the income you’re counting on. Narrow that gap, and you’re one OPEC decision – one bad quarter – away from quarterly statements that make your stomach drop.

Before you commit, know the number. It tells you more about your real risk than any projected return figure ever will.

How experienced is the operator – and what does their track record mean for your investment outcome?

Operator quality is arguably the single biggest variable in your project outcomes – more than geology, more than price environment, more certainly than the professional photography in the pitch deck.

But experience is specific. An operator with a strong track record in the Permian Basin doesn’t automatically translate that expertise to the Haynesville Shale. The geology is different. The cost structure is different. The local relationships, infrastructure, and technical demands are different.

A track record only protects your capital when it’s relevant to the project you’re actually evaluating.

What this means for you: In a direct participation investment, you don’t have a board of directors holding management accountable on your behalf. You don’t have quarterly earnings calls forcing transparency. You have the operator – their judgment, their discipline, and their experience – as your primary line of protection for your capital.

This isn’t a relationship you can exit easily if it goes wrong. Your money is committed. Getting it right before you commit isn’t a nice-to-have. It’s the most important due diligence you’ll do – because it’s protecting everything that comes after.

How does this fit into YOUR overall portfolio – and your life right now?

Oil and gas direct participation investments aren’t like stocks or bonds. They’re illiquid. They’re tied to commodity prices. They have a defined lifecycle with a beginning, a production phase, and an end.

That structure has genuine advantages – tangible cash flow you can actually use. But only if it fits where you actually are in your financial life.

The investors who get hurt in this space aren’t always in bad projects. Often they’re in reasonable projects at the wrong time – overextended, underinformed, or suddenly needing liquidity from an asset that can’t provide it. The project didn’t fail them. The fit did. And it cost them.

What this means for you: Before you commit, the question isn’t just is this a good investment? Is this the right investment for me, right now, given what else I’m holding and what I might need?

Those are different questions. The second one is harder to answer – and far more important to your financial security.

What questions should YOU still be asking?

The strongest signal that an investor is ready to commit isn’t that they’ve run out of questions. It’s that their questions have gotten sharper – more specific, more focused on protecting their capital and maximizing their actual outcomes.

At Eagle Natural Resources, we work with accredited investors who come to the table this way – with the right framework, the right questions, and a clear-eyed view of what they’re actually buying into. We respect your capital too much to avoid the hard questions.

If you’d like to walk through how we evaluate projects – and how that evaluation is designed to protect your investment from day one – we’re happy to start that conversation.

For educational purposes only. Direct investments in oil and gas carry risk, including potential loss of principal.