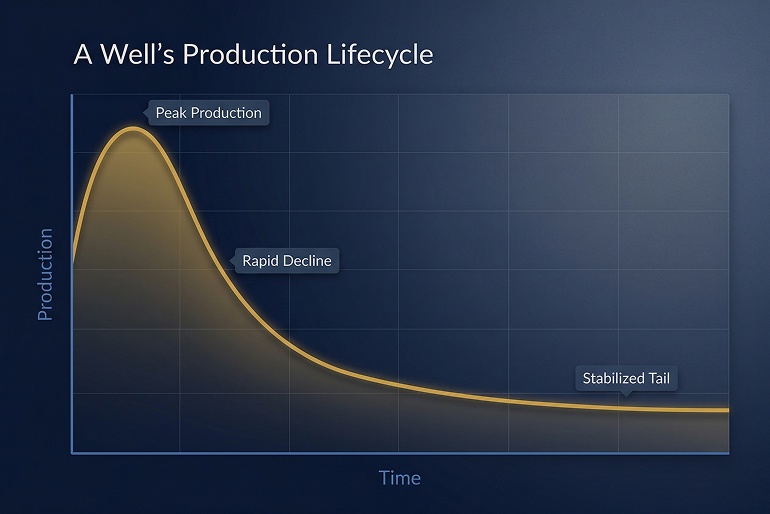

Every oil and gas well follows the same basic pattern. It comes online, produces strongly, and then – gradually – starts to slow down.

This isn’t a malfunction. It’s physics. And if you’re investing in oil and gas – or considering it – understanding this pattern is the difference between evaluating a project clearly and misreading it entirely.

What’s Happening Underground

When a well is first drilled, the pressure inside the reservoir does most of the work – pushing oil and gas toward the surface. Over time, that pressure naturally drops. As it does, so does production.

A key assumption in evaluating the expected profitability of drilling a well is the estimated ultimate recovery (EUR) of the well. Operators plan for decline from day one. It’s not an unpleasant surprise – it’s a built-in assumption that shapes every project decision, from how many wells to drill to how long a project runs.

For investors, this means the production schedule you’re shown at the start of a project isn’t a promise of a flat line. It’s a curve – and a credible operator will show you exactly what that curve looks like and how they plan to manage it.

Horizontal Wells Changed the Picture

The rise of horizontal drilling – the technique behind the U.S. shale boom – made wells significantly more productive in their early months. But it also made the decline steeper.

Horizontal wells allow operators to recover more oil and natural gas quickly after initial production begins than from vertical wells. However, horizontal wells have a high initial production rate with a steep decline relative to vertical wells.

Today, horizontal wells produce 94% of oil and 92% of natural gas in the Lower 48 states. The tradeoff is real: you get more production early, but you need to keep drilling to sustain it.

This front-loaded production profile is actually what makes early cash flow possible in many direct participation investments. The flip side is that it makes ongoing drilling activity – and the operator’s ability to execute it – critical to the project’s long-term performance.

The Treadmill Effect

This creates what operators call the “decline treadmill.” Existing wells are always losing output, so new wells have to constantly replace what’s being lost – just to stay flat.

The numbers illustrate how significant this is. In December 2023, Lower 48 crude oil production averaged 11.0 million barrels per day. Production from wells that came online in 2023 or earlier fell to 6.7 million b/d in December 2024 – a decline of 4.3 million b/d. That gap had to be filled by new drilling just to maintain production levels, let alone grow them.

For investors, this is why a project with strong early wells but no clear plan for continued drilling can plateau or disappoint. The treadmill doesn’t stop. The question is whether the operator has the capital, the acreage, and the discipline to keep pace with it.

Why This Matters for Investors

Well decline is one of the most misunderstood aspects of oil and gas investing. It can look like something going wrong when it’s actually going exactly as planned.

What it means in practice: production from a single well is finite and front-loaded. The early years generate the most output. Ongoing investment – new wells, new acreage, continued drilling activity – is what sustains and grows production over time.

This is also why operator quality matters so much. Managing decline effectively requires disciplined planning, access to quality acreage, and the technical expertise to keep bringing productive wells online. When you’re evaluating an oil and gas investment, it’s one of the most important questions you can ask: what’s the decline plan, and do they have the resources to execute it?

At Eagle Natural Resources, we work with accredited investors who want a clear-eyed view of how these projects actually work – not just the upside, but the mechanics behind it. If you’d like to learn more, we’re happy to walk you through our approach.

For educational purposes only. Direct investments in oil and gas carry risk, including potential loss of principal.