Oil and gas are often discussed in headlines, price charts, or geopolitical terms—but far less attention is paid to how private oil and gas investments actually function at an operational level. For investors who encounter the asset class through private placements or partnerships, the mechanics can feel opaque.

This article offers a plain-English overview of how private oil and gas investments are typically structured, how capital is used, how returns are generated, and what risks are involved. The goal is not to persuade, but to explain.

What “Private” Oil & Gas Investing Means

Private oil and gas investing generally refers to direct participation in individual projects or portfolios of projects, rather than buying shares of public energy companies.

These investments are usually offered through private placements, often structured as limited partnerships or limited liability companies (LLCs). Investors provide capital to fund specific oil and gas activities—most commonly drilling, completion, or acquisition of producing wells.

Unlike public stocks, private investments are:

- Not traded on exchanges

- Illiquid by design

- Structured around specific assets and timelines

Returns, when they occur, most commonly come from the cash flow generated by the underlying wells—not from buying and selling shares.

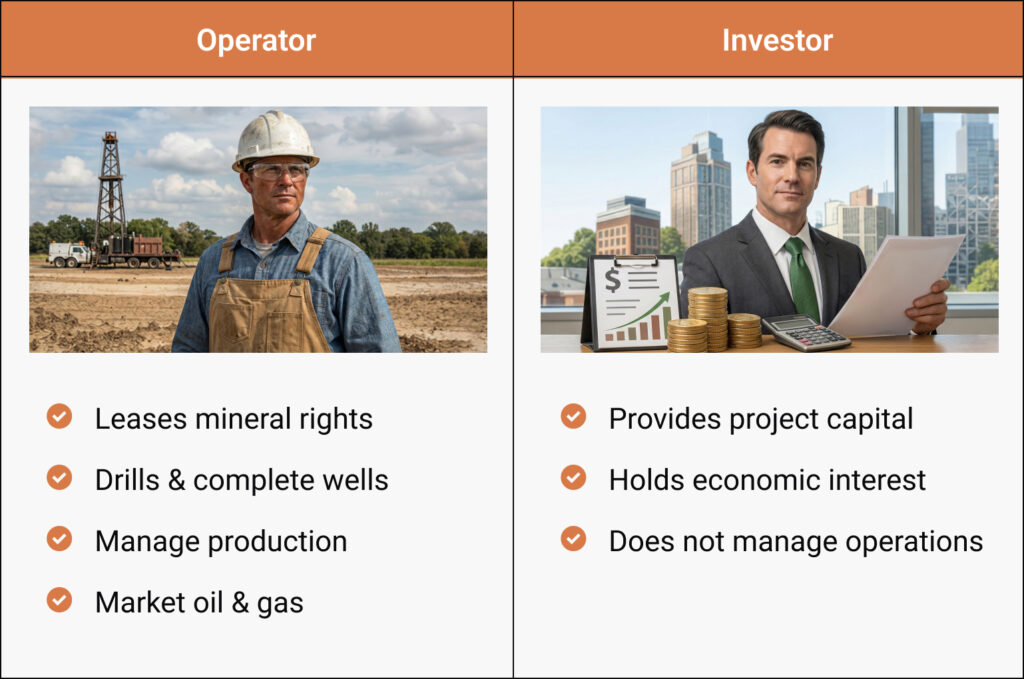

The Role of the Operator and the Investor

In a typical structure, two primary parties are involved:

The Operator

The operator is responsible for the technical and operational side of the project. This includes:

- Leasing mineral rights

- Designing and drilling wells

- Managing production and ongoing operations

- Marketing oil and natural gas

The Investor

Investors contribute capital but do not manage day-to-day operations. Their role is economic rather than operational. In exchange for funding, investors receive an ownership interest in the project and a share of revenue after expenses.

This division of responsibility allows investors to gain exposure to energy production without having to operate wells themselves.

How Capital Is Typically Used

Investor capital is usually allocated to one or more of the following:

- Drilling and Completion

Funding the physical drilling of a well and preparing it for production. - Acquisition of Producing Assets

Purchasing existing wells that are already generating cash flow. - Infrastructure and Facilities

Surface equipment, pipelines, or processing infrastructure tied directly to production. - Operating and Administrative Costs

Ongoing expenses required to keep wells producing.

Capital is often deployed early in the life of the investment, particularly in drilling-focused projects.

From the Ground to Revenue: How Cash Flow Is Generated

Once a well begins producing, oil or natural gas is sold into the market. Revenue flows through several steps:

- Production – Oil or gas is extracted from the well

- Sales – Production is sold to purchasers at prevailing market prices

- Deductions – Operating expenses, taxes, and royalties are paid

- Distributions – Remaining cash is distributed to owners based on their interest

Investor returns are therefore tied to:

- Production volumes

- Commodity prices

- Operating efficiency

- Decline rates over time

Unlike some growth-oriented assets, many private oil and gas investments are often evaluated primarily on their ability to generate ongoing cash flow.

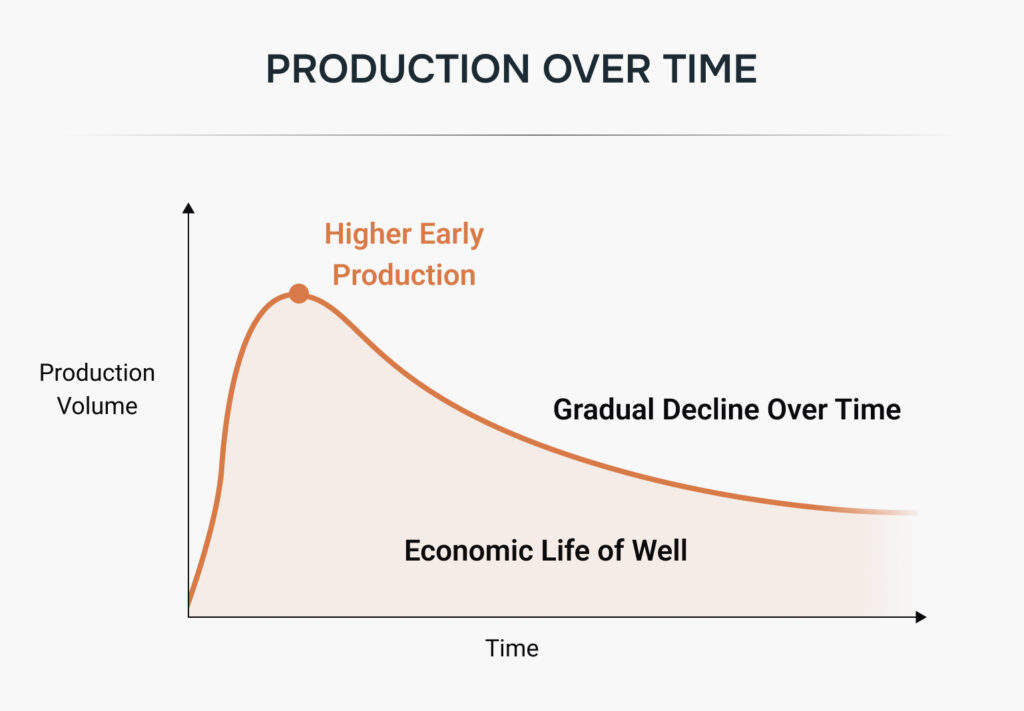

Understanding Time Horizons and Decline

Oil and gas wells do not produce at a constant rate forever. Most wells experience:

- Higher production early in life

- Gradual decline over time

Because of this, private oil and gas investments are typically structured with a defined economic life. Some may emphasize:

- Shorter-term cash flow, or

- Longer-term development potential, depending on the strategy

Understanding the expected production curve is central to understanding the investment itself.

Risks and Tradeoffs to Consider

As with any real asset investment, oil and gas involves meaningful risk. Common considerations include:

- Commodity price volatility – Revenue depends on oil and gas prices

- Geologic risk – Wells may underperform expectations

- Operational risk – Costs, downtime, or mechanical issues can impact results

- Illiquidity – Capital is typically committed for multiple years

These risks are why oil and gas investments are often discussed in terms of suitability and portfolio role, rather than as standalone solutions.

How This Differs From Public Energy Stocks

It’s important to distinguish private oil and gas investments from public energy equities:

| Private Oil & Gas | Public Energy Stocks |

| Asset-level exposure | Company-level exposure |

| Cash flow driven | Share price driven |

| Illiquid | Highly liquid |

| Project-specific | Broad corporate operations |

Neither structure is inherently better—they simply function differently and are used differently by investors.

A Grounded View of the Asset Class

Private oil and gas investing is best understood as participation in physical energy production. Capital funds real assets, returns come from real output, and results depend on geology, execution, and market conditions.

For those exploring the space, clarity around structure and mechanics is essential. Understanding how these investments work provides a foundation for asking better questions—about risk, alignment, and expectations—before any capital is committed.

Resources

For readers who want to explore the mechanics of oil and gas operations and investment structures in more detail, the following sources provide neutral, educational context:

- U.S. Energy Information Administration (EIA)

Overview of oil and natural gas production, pricing, reserves, and industry structure. - Bureau of Land Management (BLM)

Information on onshore oil and gas leasing, development, and regulation on federal lands. - Internal Revenue Service (IRS)

General guidance on partnerships, pass-through entities, and natural resource taxation. - Society of Petroleum Engineers (SPE)

Educational resources on drilling, production, reservoir behavior, and decline characteristics. - State oil and gas regulatory agencies (e.g., Texas Railroad Commission, Oklahoma Corporation Commission)

Operational and regulatory context at the state level.

These resources are provided for general education and independent research. They are not intended as market forecasts or investment guidance.