For high networth accredited investors ONLY:

Receive HUGE tax breaks while you sit back and collect mailbox money every month with tangible asset ownership in oil & gas investment opportunities.

Why Investors Join The Investor Portal:

- Write off up to nearly 85% of your investment in the first year.

- Significant earning potential with oil & gas revenue

- Reinvest tax savings for compound income

-

Hedge against inflation & diversify your portfolio (not volatile like

the stock market) - Tangible asset ownership through joint ventures

- Straight-forward participation. No hidden fees

TANGIBLE ASSET OWNERSHIP*

You own interest in oil and natural gas wells, not energy company stocks that are at the mercy of an unpredictable market.

GENEROUS TAX BENEFITS

Minimize your tax liability with a write-off of up to nearly 85% of your investment in the first year.

OIL AND GAS REVENUES

Now is the time to buy oil and gas assets. Thanks to record breaking growth & consumption, and lower drilling & operational costs, you’re positioned well for strong returns.

Your Potential Write-Offs in Year One:

Based on a $100,000 Investment* with Eagle Natural Resources

Intangible Drilling

Cost Tax Deduction

Enjoy up to $80,000 in IDC tax deductions during the 1st year of the venture.

The intangible expenditures of drilling (labor, chemicals, mud, grease, etc.) are usually about (65 to 80%) of the cost of a well. These expenditures are considered “Intangible Drilling Cost (IDC)” and are available in the year the money was invested, even if the well does not start drilling until March 31 of the year following the contribution of capital. (See Section 263 of the Tax Code.)

Tangible Drilling

Cost Tax Deduction

Generate an additional $2,800 in TDC, bringing the total write-off potential in Year 1 to $82,800.

The total amount of the investment allocated to the equipment “Tangible Drilling Costs (TDC)” is 100% tax-deductible. In the example above, the remaining tangible costs may be deducted as depreciation over a seven-year period. (See Section 263 of the Tax Code.)

*Fractional investment units available; $50,000 min investment

How it works

Most oil and gas investments are overly complex. We’ve spent over 10years simplifying our direct participation approach to help high-income earners like you invest with confidence.

IDENTIFY

Eagle’s acquisition model focuses on Proved Undeveloped (PUD) drilling locations in proven producing fields; no risky wildcatting.

These fields have extensive infrastructure, existing wells for immediate cash flow, and upside through additional drilling, recompletion and/or rework operations.

ACQUIRE

We do Extensive third-party geophysical/economic due diligence on all acquisitions.

By targeting financially-distressed energy assets, they will benefit immediately from operational improvements paid for with an infusion of capital.

This provides us with the potential to deliver our investors solid returns in minimum time.

DEVELOP

We have a turn-key development plan that quickly and methodically increases performance potential.

From simple mechanical reworks and replacing old equipment to fracking existing wellbores.

Our goal is to drive an approximate 200 to 400 percent increase in production through targeted development.

EARN

For existing producing assets, investors typically receive their first revenue check within 90 to 120 days.

For new drilling, distributions typically begin 60 days after a well begins producing.

Long term, you can rest easy knowing that Eagle’s management team is overseeing all aspects of operations.

Why Now

*Fractional investment units available; $50,000 min investment

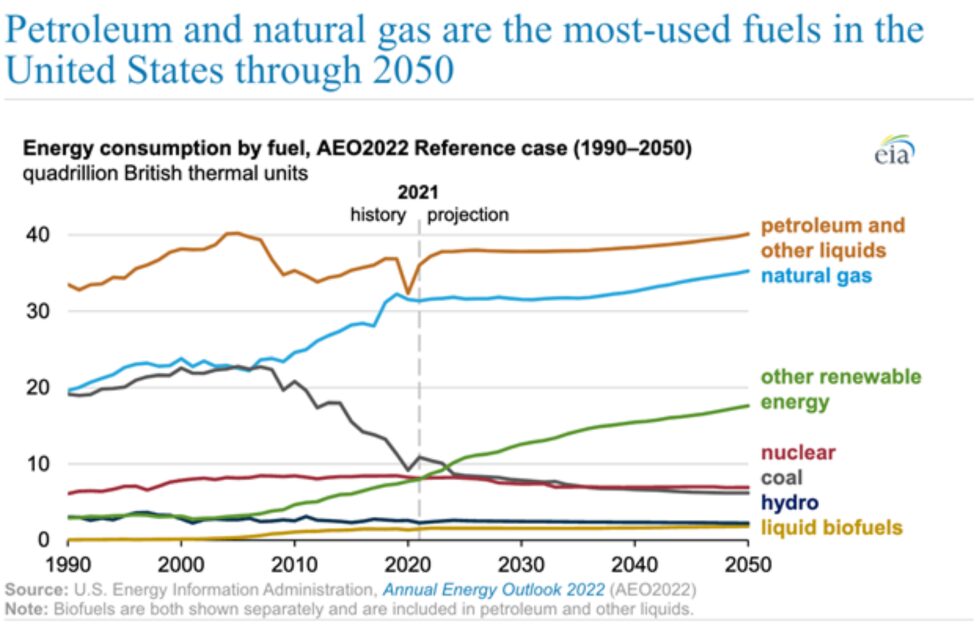

Record-Breaking Production & Record-Breaking

Consumption for Record-Breaking Profits.

BOTH the production and demand for oil are set to break records and will continue to rise to all-time highs in 2025.

U.S. crude oil production is forecasted to average 13.1 million barrels per day in 2025, slightly below the anticipated 2024 peak but still maintaining record-high levels, showcasing the resilience and strength of American energy production.

In 2025, the EIA forecasts an encouraging uptrend in global energy consumption, with petroleum and other liquid fuels expected to see a demand increase of 1.7 million barrels per day, driven by recovering economic activity and sustained growth in emerging markets.

Additionally, natural gas consumption is projected to grow steadily in 2025, bolstered by its increasing adoption in power generation and industrial sectors worldwide. This trend reflects the vital role of natural gas as a transitional energy source in a diversifying global energy landscape.

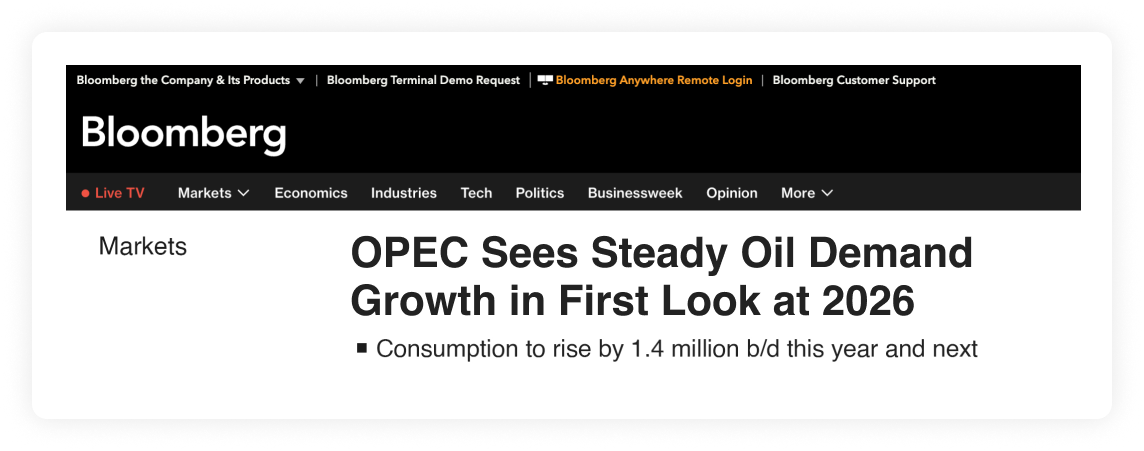

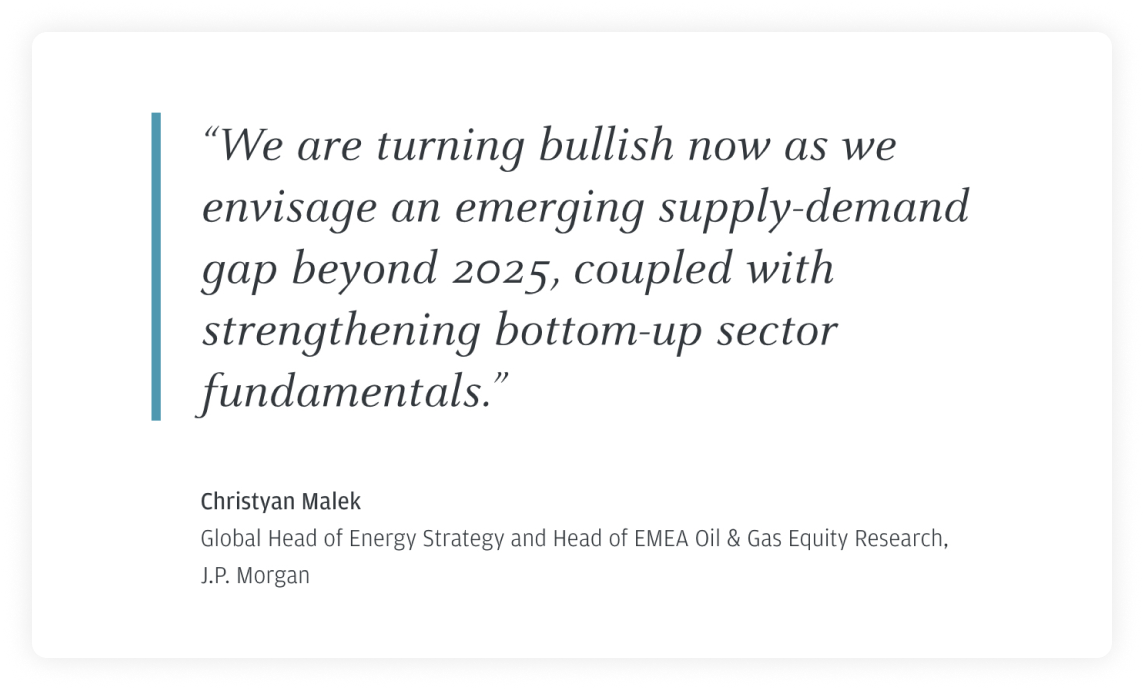

Goldman Sachs Predicts We’re Still a Decade Away

From Peak Demand

J.P. Morgan Are Just As Bullish

When Demand Increases Oil Prices Have Always

Trended Up Over Time (Despite Short-Term Volatility)

While there have been short-term dips, the overall trend is clear: oil prices

consistently rise over the years.

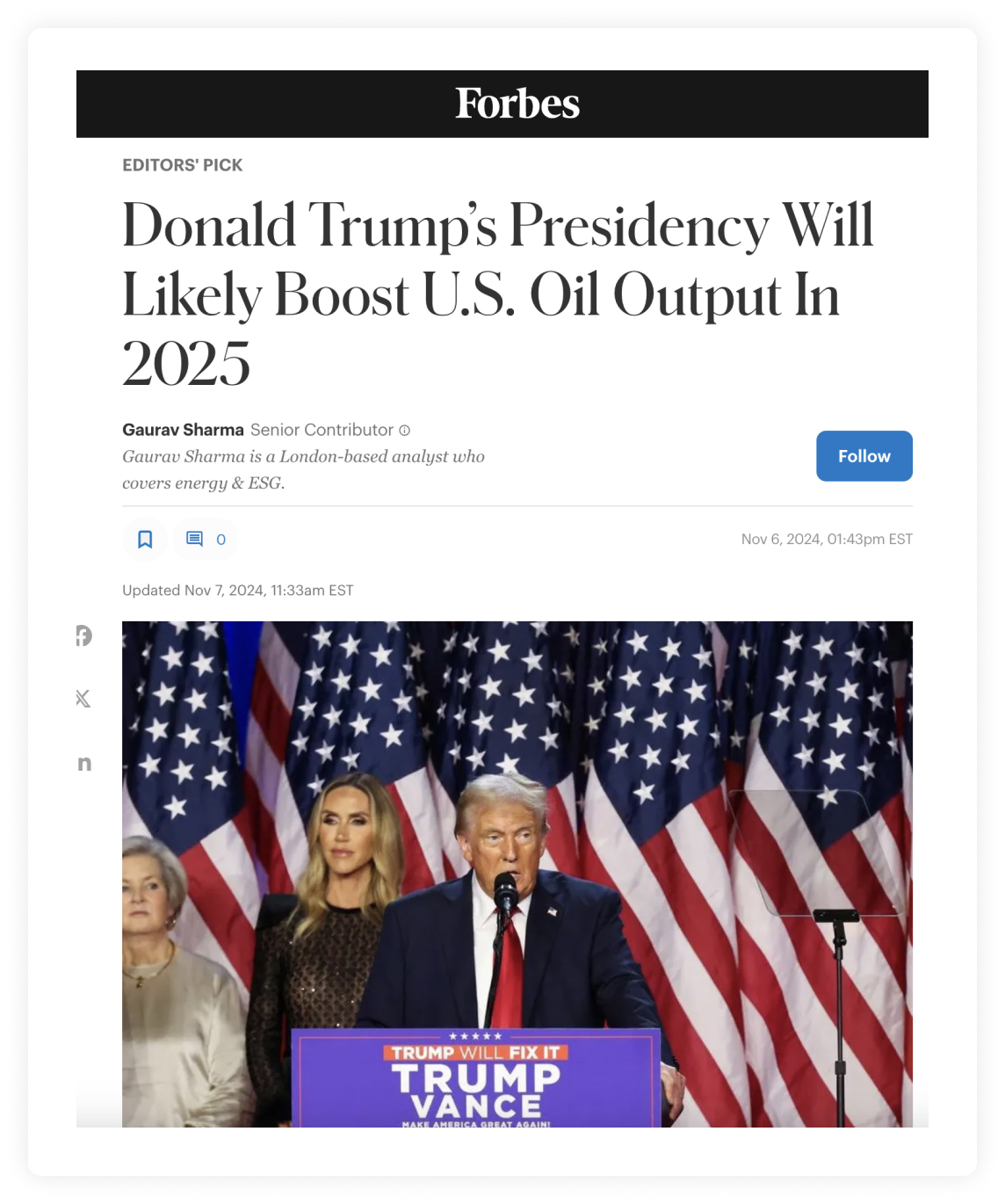

Plus Output Is Set to Increase Under

the Trump Administration

High Demand + High Oil Prices = An Opportunity That Has Never Been Greater For Real Property Oil & Gas Investing

Will You Be a Part of It?

Finally, an investment you can explain to a friend,point

your finger on a map, and say,

“That’s exactly where my money is,

and here’s why.”

- We focus on Proved Undeveloped (PUD) drilling locations in proven producing fields with zero wildcatting.

- Extensive third-party geophysical/economic due diligence

- Diversification: Rather than invest in one well, we spread the investment dollars over three to six wells, greatly reducing the impact of a failed well. The idea being the good wells will make up for the bad

- Our experienced management facilitates all phases of upstream operations.

- Partner K1s are dispersed annually directly from Eagle.

- Straight-forward, easy-to-understand participation with zero hidden fees

- Tangible asset ownership: You own interest in oil and natural gas wells via joint ventures

- Generous Tax Benefits: Minimize your tax liability with a write-off of up to 85% of your investment.

- Potential for significant returns with oil and gas revenues

- Existing cash flow from producing wells

- Lower risk drilling and development

- Upside potential through targeted improvements and drilling

Our Portfolio

- $125MM+ assets under management

- 250+ PUD Locations under lease with 376 producing wells across 95,000+ acres

- 68+ MMBO and 518+ MCFG produce

Frequently Asked Questions

An investment in an Oil & Gas Direct Participation Fund such as the Fund, allows investors to participate directly in the Fund’s cash flow, which is generated by the oil and gas assets owned by the Fund. In addition, some investors may enjoy the tax benefits generated by the Fund’s activities, which could potentially be used to help reduce the individual investor’s tax burden.

Accredited investors seeking (1) to generate income along with opportunities for upside growth, (2) direct exposure to profit potential generated by oil and gas operations, and (3) tax advantages, may find that an investment in the Fund is an attractive diversification option to an existing investment strategy. Investors should note that oil and gas direct investing carries significant risk and there are no guarantees that any cash flow will be achieved. Please review the offering documents relating to any investment opportunity being evaluated in full prior to making an investment including specifically any Risk Factors identified therein. ACCREDITED INVESTORS ONLY

Eagle’s acquisition model focuses on proven-producing fields with existing infrastructure and wells expected to generate immediate cash flow and potential upside through additional drilling operations. We plan to primarily target the acquisition of financially distressed energy assets that may immediately benefit from operational improvements paid for with an infusion of capital. This sets the stage for an attractive arbitrage opportunity on the buy-side, which could maximize our Funds’ overall return potential. In addition, through our wholly-owned subsidiary ENR Operating we are able to better control costs by directly negotiating and managing required oilfield services.

Yes. Non-U.S. residents may invest in Eagle’s Fund, subject to local securities laws.

If the Fund’s revenues exceed its expenses, investors are expected to receive periodic distributions of the Fund’s cash profits. Eagle expects that cash distributions to the partners will begin approximately three months after the Fund acquires or drills, completes and hooks up its first producing well, and may be made as frequently as monthly thereafter, but in any event, no less than quarterly. The distribution amount will depend primarily on the Fund ‘s net cash receipts from oil and natural gas operations and will be affected, among other things, by the price of oil and natural gas and the level of production of the Fund’s properties.

There are restrictions in transferring ownership of units in the Fund; Ownership in the Fund is not a liquid investment. No public market for the units exists or is likely to develop. You should be fully aware of the long-term nature of an investment in the Fund. Investors will be required to represent that they are purchasing units in the Fund for their own account for investment purposes and not with a view toward resale or redistribution. The sale of the Fund units will not be registered under the Securities Act, and the units must be held indefinitely unless they are subsequently registered under the Securities Act (which is not expected) or unless an exemption from registration is available. Resale of the units under Rule 144 of the Securities Act within one year from the date they are fully paid will not be possible because of the absence of sufficient public information about the Partnership. Furthermore, you may not transfer your units except as expressly permitted in the Fund’s partnership agreement

Oil and gas direct investing offers many tax advantages that can help greatly enhance the economics of an investment. The following information and Internet URL are provided for your convenience and should not be construed as tax advice from Eagle. It is the responsibility of each PARTNER to investigate the tax consequences, under the laws of pertinent jurisdictions, of his or her investment in the FUND. THE ANALYSIS HEREIN IS NOT INTENDED AS A SUBSTITUTE FOR CAREFUL TAX PLANNING. ACCORDINGLY, EACH PROSPECTIVE INVESTOR IS URGED TO CONSULT WITH HIS OWN PERSONAL TAX ADVISOR CONCERNING (i) THE APPLICABILITY TO AND EFFECT ON HIM OF THE UNITED STATES INCOME TAX LAWS AND THEIR ADMINISTRATION, AND (ii) THE APPLICABILITY TO AND EFFECT ON HIM OF STATE, LOCAL AND FOREIGN TAX LAWS AND THEIR ADMINISTRATION. NO LAW FIRM OR ACCOUNTING FIRM HAS PROVIDED OR OTHERWISE Rendered an opinion on the FEDERAL, state, local or foreign tax consequences of an investment in THE FUND. The Online U.S. Tax Code may be accessed at http://www.fourmilab.ch/ustax/ustax.html

Intangible Drilling Cost Tax Deduction

The intangible expenditures of drilling (labor, chemicals, mud, grease, etc.) are usually about (65 to 80%) of the cost of drilling an oil and/or gas well. These expenditures are considered “Intangible Drilling Cost (IDC)”, which may be 100% deductible during the first year for certain qualifying investors. For example, a $100,000 investment could yield up to $80,000 in IDC tax deductions during the first year of the venture. These deductions are generally available in the year the money was invested, even if the well does not start drilling until March 31 of the year following the contribution of capital. (See Section 263 of the Tax Code.)

Tangible Drilling Cost Tax Deduction

The total amount of the investment allocated to the equipment “Tangible Drilling Costs (TDC)” is 100% tax deductible. In the example above, the remaining tangible costs ($20,000) may be deducted as depreciation over a seven-year period. (See Section 263 of the Tax Code.)

Active vs. Passive Income

The Tax Reform Act of 1986 introduced into the Tax Code the concepts of “Passive” income and “Active” income. The Act prohibits the offsetting of losses from Passive activities against income from Active businesses. The Tax Code specifically states that a Working Interest in an oil and gas well is not a “Passive” Activity. (See Section 469(c)(3) of the Tax Code). As such, if the Fund owns one or more working interests in one or more oil or gas leases at any time during a tax year, individual investors that own general partnership interests directly or through entities that do not limit their liabilities with respect to their units should not be subject to the passive activity loss rules with respect to such working interests for the tax year. As a result, such investors should be able to utilize losses from the Fund from such working interests to offset future income from the Fund and their other so-called “active income” (e.g., salary) and “portfolio income” (e.g., dividends, interest and royalties not derived in the active conduct of a trade or business).

Small Producers Tax Exemption

The 1990 Tax Act provided some special tax advantages for small companies and individuals. This tax incentive, known as the “Percentage Depletion Allowance”, is specifically intended to encourage participation in oil and gas drilling. This tax benefit is not available to large oil companies, retail petroleum marketers, or refiners that process more than 50,000 barrels per day. It is also not available for entities owning more than 1,000 barrels of oil (or 6,000,000 cubic feet of gas) average daily production. The “Small Producers Exemption” allows 15% of the Gross Income (not Net Income) from an oil and gas producing property to be tax-free.

Lease Costs

Lease costs (purchase of leases, minerals, etc.), sales expenses, legal expenses, administrative accounting, and Lease Operating Costs (LOC) are also 100% tax deductible through cost depletion.

At the expense of the Fund, Eagle will engage a certified public accountant to prepare the Fund’s annual income tax return and the return required by Internal Revenue Code section 6050K relating to sales and exchanges of interests in the Fund. Within a reasonable time after the close of each accounting year, Eagle will transmit to each person who was a partner during such accounting year a report (which may be in the form of Schedule K-1 to IRS Form 1065) indicating such person’s respective share of profits, losses and other federal income tax items, tax preference items and investment credits, if any, for such year. Eagle will also furnish to the Fund’s investor partners a report containing an overview of operations on at least an annual basis.

There are significant risks associated with oil and gas investments. One of the biggest risks is the fact that commodities pricing can be volatile. Cash flow potential varies according to two main variables: the amount of gas or oil that is produced and sold (if any) and the price that is received for the gas or oil. Both of these variables can fluctuate based on a range of different factors; for example, the price of oil can rise or fall dramatically due to political or economic issues, or even due to the weather.

Gas and oil wells are also depleting assets. The typical production life of an oil well could span between up to twenty and thirty years. Nevertheless, dry holes are possible and returns can decline after the first couple of years. Sometimes the property or wells are made ‘for sale’ a few years down the line, other times they might not be. If there is a proposed exit strategy for the investment that you are considering, it is important that you fully understand it.

As a working interest owner in the various properties in which it invests, the Fund is liable for the debts and obligations to third parties incurred by the operator in conducting operations on an oil and gas lease to the extent of their proportionate working interests. In general, the liability of an owner of a fractional undivided working interest includes contract liability, tort liability, special statutory liability and tax liability.

External political and external events also affect gas and oil availability and pricing. There are varying levels of risk among energy choices. You should consider all energy choices as high risk but royalty programs generally tend to be more conservative while experimental drilling programs are the most speculative. Drilling operations may also result in a dry hole, in which case all amounts invested in such operations could be lost.

It is important to remember that your risks are directly tied to those of the company that is in charge of managing your investment. You should therefore ensure that you know the history and background of this company and carry out due diligence before you opt to invest

With a focus on delivering both income and growth potential, ENR Income & Development Partnerships may be a smart fit for investors seeking to diversify into domestic energy production.

About Us

Eagle Natural Resources is a privately held oil and gas operating company based in Texas. We offer accredited investors direct access to U.S. energy projects focused on long-term value, transparency, and responsible development.

SITEMAP

Contact

Eagle Natural Resources, LLC

RRC # 253075

5445 Legacy Dr. STE 440 Plano TX 75024

Phone: (833) 553-1534

There are significant risks associated with oil and gas investments. Information found on this site is for general purposes only and is not a solicitation to buy or an offer to sell securities. General information on this site is not intended to be used as individual investment or tax advice. Consult your personal tax advisor concerning the current tax laws and their applicability and effect on your personal tax situation.